Operating vs. Capital Expenses: A Farmer’s Guide to Deductions

Tax season can be a daunting time for farmers, especially when it comes to understanding the nuances of deductions. Knowing the difference between operating and capital expenses is crucial for maximizing tax savings and ensuring compliance with IRS regulations. This guide will break down these categories and provide examples to help you confidently categorize your farm expenses.

Don’t worry about sounding professional. Sound like you. There are over 1.5 billion websites out there, but your story is what’s going to separate this one from the rest. If you read the words back and don’t hear your own voice in your head, that’s a good sign you still have more work to do.

Be clear, be confident and don’t overthink it. The beauty of your story is that it’s going to continue to evolve and your site can evolve with it. Your goal should be to make it feel right for right now. Later will take care of itself. It always does.

What are Operating Expenses?

Operating expenses are the short-term, recurring costs directly related to the day-to-day running of your farm. These are fully deductible in the year they are incurred, reducing your taxable income and ultimately your tax liability.

Here are some common examples of operating expenses for farmers:

Feed, seed, fertilizer, and other supplies: The essential inputs for crop and livestock production.

Repairs and maintenance: Keeping your farm equipment and facilities in working order, such as fixing a tractor or repairing a fence.

Fuel and utilities: The energy costs associated with running your farm operations.

Labor: Wages paid to employees, including hired help for planting, harvesting, or livestock care.

Rent or lease payments: For land, buildings, or equipment used in your farming activities.

Property taxes: The annual taxes assessed on your farmland and buildings.

Insurance premiums: Protecting your farm assets, crops, and livestock from unforeseen events.

Marketing and advertising: Promoting your farm products and reaching potential customers.

Veterinary and breeding expenses: Healthcare for livestock, including vaccinations, medications, and breeding services.

What are Capital Expenses?

Capital expenses are investments in long-term assets that will benefit your farm for more than one year. These expenses are not fully deductible in the year of purchase. Instead, they are depreciated over their useful life, meaning you deduct a portion of the cost each year.

What’s the Difference?

The difference between operating expenses (tending crops) and capital expenses (buying a tractor).

Here are some common examples of capital expenses for farmers:

Purchase of farm equipment: Tractors, combines, plows, and other machinery essential for large-scale farming.

Construction or major improvements to buildings: Building a new barn or significantly renovating an existing structure.

Land purchases: Expanding your farm operation by acquiring additional acreage.

Breeding livestock: Investing in high-quality animals to improve your herd genetics.

Depreciation and Section 179

Depreciation is a critical concept for capital expenses. It allows you to deduct a portion of the asset’s cost each year, spreading the expense over its useful life. This can help you manage your tax liability more effectively and recover the cost of your investment over time.

Section 179 is a tax provision that allows farmers to fully or partially deduct the cost of eligible capital expenses in the year they are placed in service. This can provide a significant tax advantage, allowing you to accelerate depreciation and reduce your taxable income in the year of purchase. However, Section 179 has specific limits and qualifications, so consult with a tax professional to determine your eligibility.

Why is Distinguishing Between Operating and Capital Expenses Important?

Correctly classifying expenses as operating or capital has several implications for your farm taxes:

Deduction timing: Operating expenses are deductible immediately, providing a faster tax benefit. Capital expenses are depreciated over time, leading to a slower but still valuable tax benefit.

Tax liability: Misclassifying capital expenses as operating expenses can lead to overstating your deductions and underpaying your taxes, potentially resulting in penalties.

Financial planning: Understanding the depreciation schedule for capital assets helps you project future tax liabilities and make informed financial decisions for your farm.

Tips for Accurate Expense Classification

Here are some tips to ensure you correctly classify your farm expenses:

Maintain detailed records: Keep receipts, invoices, and other documentation for all your expenses.

Use accounting software: Farm-specific accounting software can help you categorize expenses accurately and generate reports for tax filing.

Consult a tax professional: A qualified tax advisor with experience in agricultural businesses can guide you on complex expense classifications and ensure you're taking advantage of all available deductions.

Conclusion

By understanding the difference between operating and capital expenses, you can make informed decisions about your farm finances and optimize your tax strategy. Accurate expense classification is crucial for minimizing your tax liability, avoiding penalties, and ensuring the long-term financial health of your farm. Remember to maintain meticulous records, utilize accounting tools, and seek professional guidance when needed. With these strategies, you can confidently navigate tax season and keep more of your hard-earned income.

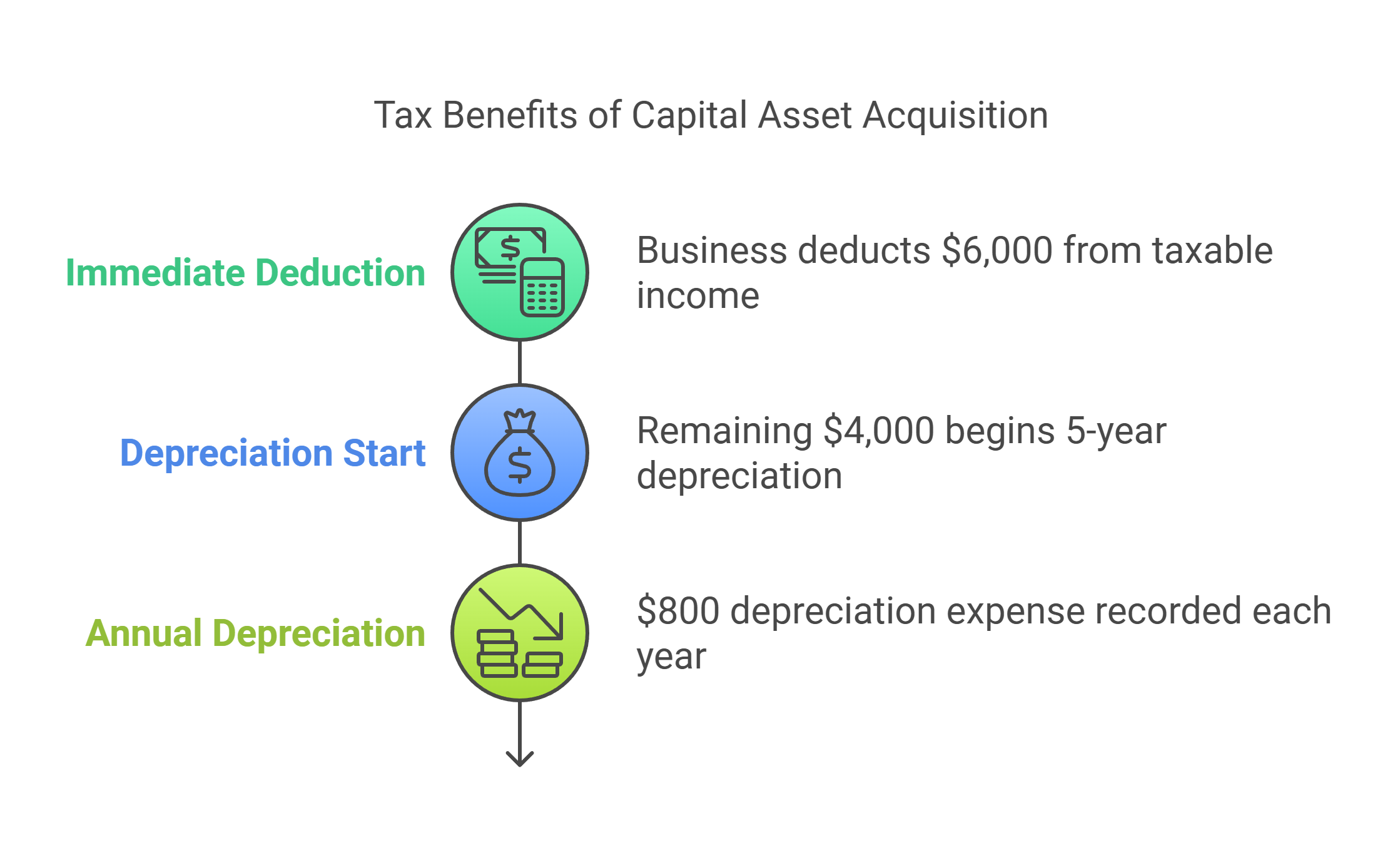

Total Cost: The total cost of the capital asset is $10,000.

Immediate Deduction: Under Section 179, the business can deduct $6,000 immediately from its taxable income.

Remaining Cost: The remaining $4,000 is subject to depreciation.

Depreciation: This amount can be depreciated over a period of 5 years, resulting in an annual depreciation expense of $800.